- Can You Really Get a 10000 Loan Using Only Aadhar Card?

- Who Can Apply for a 10000 Loan on Aadhar Card?

- Basic Requirements You Should Know Before Applying

- Best Ways to Get a 10000 Loan Using Aadhaar

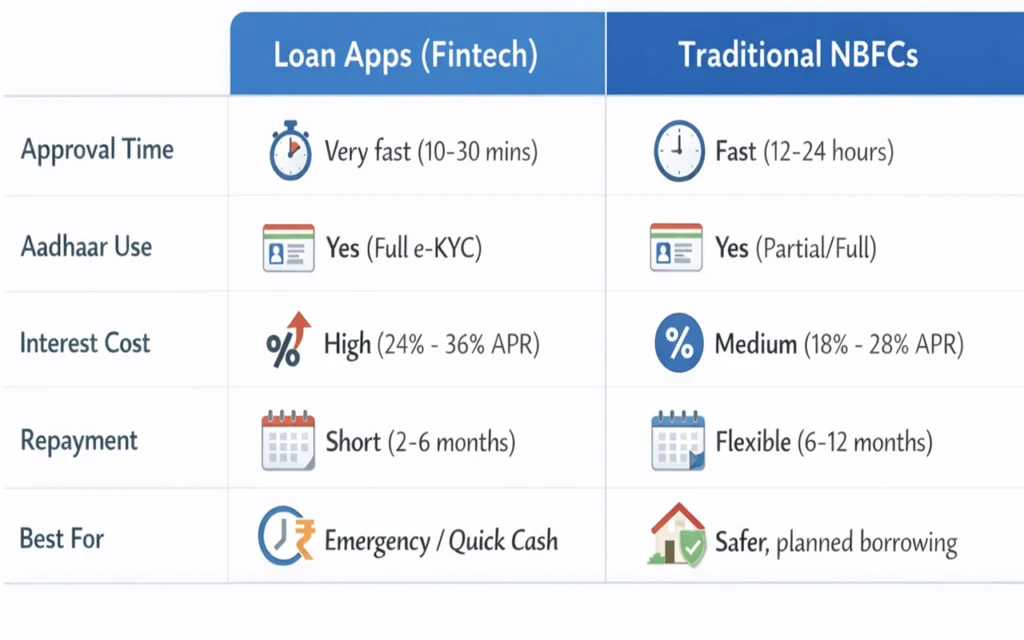

- App Loans vs NBFC Loans (Quick Comparison)

- Real Cost of a 10000 Loan (People Ignore This)

- Common Mistakes People Make While Taking Small Loans

- Is a 10000 Aadhaar Loan Safe for Your Credit Score?

- When You Should Avoid Taking This Loan

- Better Alternatives to a 10000 Loan

- Questions People Ask About 10000 Loan on Aadhaar Card (FAQ)

- Avinash’s Honest Advice

Last Updated: January 15, 2026 (Eligibility rules, calculator)

You’re likely here because you need ₹10,000 quickly, and you’ve heard that your Aadhaar card is the magic key to instant cash. Maybe it’s a mid-month cash crunch, a sudden repair, or a small medical bill. Whatever the reason, the search for a 10000 loan on Aadhar card is one of the most misunderstood topics in Indian finance today.

I’m Avinash, and after a decade in the lending industry, I’ve seen the “instant loan” market grow from a few niche players to a crowded digital jungle. I’ve seen people get their money in 5 minutes, but I’ve also seen many fall into deep debt traps because they didn’t understand the fine print.

In this guide, I’m going to cut through the marketing fluff. I’ll tell you exactly what is possible, what is a myth, and how to protect your financial health while getting a 10000 loan on Aadhar card.

Can You Really Get a 10000 Loan Using Only Aadhar Card?

The short answer is: No, not strictly “only” your Aadhaar. Let’s break down why lenders use this document and where the confusion starts.

Why lenders ask for Aadhaar

Lenders love Aadhaar because of e-KYC. It allows them to verify your identity and address instantly via an OTP. This speed is what makes the 10000 loan on aadhar card feel “instant.”

Why Aadhaar alone is not enough

Think of Aadhaar as your digital handshake. It tells the lender who you are, but it doesn’t tell them if you can pay back. To decide that, they need to see your income. In 2026, lenders use the Account Aggregator framework to peek at your bank transactions. Without this “digital proof of income,” an Aadhaar card is just a plastic card.

PAN vs Aadhaar role (simple explanation)

If Aadhaar is your ID, your PAN (Permanent Account Number) is your financial resume. For any 10000 loan on aadhar card, the lender will almost certainly ask for your PAN to check your credit history (CIBIL).

Myth Buster: If an app claims to give you a 10000 loan on aadhar card without asking for your PAN or checking your credit history, run away. These are often unregulated “Chinese apps” that use predatory tactics.

Who Can Apply for a 10000 Loan on Aadhar Card?

Different lenders have different “risk appetites.” Here is how the market views you based on your profile:

Salaried users

If you have a fixed salary credited to your bank account, you are the “Gold Standard.” Lenders will give you a 10000 loan on aadhar card with the lowest interest rates because your repayment capacity is predictable.

Self-employed users

Shopkeepers or freelancers often struggle with traditional banks. However, modern fintech apps look at your UPI transaction patterns. If your shop’s QR code gets regular payments, getting a 10000 loan on aadhar card becomes much easier.

First-time borrowers

If you’ve never taken a loan, you have low CIBIL score. You might face slightly higher interest rates initially, but a small 10000 loan on aadhar card is actually a great way to start building your credit history.

Low CIBIL or no CIBIL users

Don’t believe the “100% Approval” lies. If your score is below 600, most major banks will reject you. Your best bet for a 10000 loan on aadhar card would be NBFC-backed apps like TrueBalance or mPokket, which prioritize your current “banking discipline” over past credit mistakes.

Basic Requirements You Should Know Before Applying

Before you click ‘Apply’ on any app for a 10000 loan on aadhar card, make sure you have these four things ready. If even one is missing, you’ll likely face a “Technical Rejection.”

- Aadhaar-linked mobile number: You will need to sign your loan agreement digitally via an OTP sent to the mobile number registered with UIDAI.

- PAN requirement: In 2026, RBI regulations have made it nearly impossible for regulated lenders to skip the PAN check for a 10000 loan on aadhar card.

- Bank account conditions: You need a “Live” savings account with net banking or a debit card. This is required to set up an e-NACH (National Automated Clearing House) mandate so your EMIs can be auto-deducted.

- Income or transaction pattern: Even if you don’t have a salary slip, your bank statement should show regular “Inward” transactions.

Best Ways to Get a 10000 Loan Using Aadhaar

You have three main paths to get this money. Each has its own pros and cons.

Instant loan apps (when they work)

Apps like KreditBee, Navi, and Fibe are the fastest. They are built for the 10000 loan on aadhar card niche. They use AI to scan your profile and can disburse money in as little as 10 minutes.

NBFC small-ticket loans

Companies like Tata Capital or L&T Finance have specific products for small amounts. These are often safer and have slightly lower interest rates than apps, but the process might take 24–48 hours.

Credit line based loans

Apps like StashFin or Olyv (SmartCoin) give you a “Credit Line.” You get approved for, say, ₹50,000, but you only take a 10000 loan on aadhar card. You only pay interest on the ₹10,000 you actually use.

Why banks usually avoid small loans

You might wonder why HDFC or ICICI doesn’t market a 10000 loan on aadhar card. The truth is, the administrative cost of processing a ₹10,000 loan is almost the same as a ₹5 Lakh loan. For big banks, small loans aren’t profitable enough.

App Loans vs NBFC Loans (Quick Comparison)

Choosing the right platform for your 10000 loan on aadhar card depends on your priority: Speed vs. Cost.

Real Cost of a 10000 Loan (People Ignore This)

Lenders often hide the true cost of a 10000 loan on aadhar card behind low “monthly” interest rates. Let’s do the math.

- Interest impact: A “3% monthly” rate sounds small, but that is 36% per year.

- Processing fee: Most apps charge between ₹200 and ₹500 upfront. If you get a 10000 loan on aadhar card, you might only receive ₹9,500 in your bank account.

- Short tenure trap: If you take the loan for only 30 or 60 days, the processing fee makes the “Effective Interest Rate” massive.

- EMI pressure example: For a ₹10,000 loan at 30% APR for 3 months, your EMI will be roughly ₹3,500. Can your monthly budget handle an extra ₹3,500 outflow?

Underground Tip: Always check the APR (Annual Percentage Rate). It is a legal requirement for lenders to show this. It tells you the total cost of the 10000 loan on aadhar card including all fees.

Common Mistakes People Make While Taking Small Loans

I’ve seen many smart people ruin their financial future over a tiny 10000 loan on aadhar card. Avoid these four traps:

- Applying on too many apps: Every time you apply, it’s a “Hard Inquiry” on your CIBIL. Apply on 5 apps at once, and your score will drop 20-30 points instantly.

- Ignoring repayment date: These apps are ruthless. A one-day delay in your 10000 loan on aadhar card repayment can lead to heavy penalties and dozens of automated collection calls.

- Trusting “no document” claims: If it sounds too good to be true, it is. Regulated lenders must document their loans.

- Rolling loans: Never take a second loan to pay off your first 10000 loan on aadhar card. This is the beginning of a debt spiral that is very hard to escape.

Is a 10000 Aadhaar Loan Safe for Your Credit Score?

A 10000 loan on aadhar card is a double-edged sword for your CIBIL score.

- Impact if paid on time: It’s excellent. It shows you are a responsible borrower. This “Credit Mix” helps you get bigger Home or Car loans later.

- Impact if delayed: Even a 3-day delay is reported to credit bureaus. It can stay on your record for 7 years.

- How it affects future loans: Banks look at your “Enquiries.” If they see you’ve taken ten 10000 loan on aadhar card requests in a year, they see you as “Credit Hungry” and may reject your Home Loan.

When You Should Avoid Taking This Loan

As a mentor, I often tell people not to take a loan. You should avoid a 10000 loan on aadhar card if:

- Your income is unstable: If you aren’t sure you’ll have the EMI money next month, don’t borrow.

- EMIs are already running: If 50% of your income already goes into debts, a new 10000 loan on aadhar card will break your budget.

- Using for non-urgent spending: Never borrow at 30% interest to buy a new phone or party. It’s financially suicidal.

Better Alternatives to a 10000 Loan

Before you commit to a 10000 loan on aadhar card, check these options:

- Salary advance: Ask your HR. Many companies have a policy for interest-free advances.

- Credit card cash option: If you have a card, checking the “Cash Limit” might be cheaper than a fresh loan app fee.

- Small gold loan: If you have a gold chain or ring, a gold loan is 50% cheaper in interest than an app-based 10000 loan on aadhar card.

- Borrow from friends/family: It might be awkward, but it saves you from interest and credit score risks.

Questions People Ask About 10000 Loan on Aadhaar Card (FAQ)

Is PAN compulsory for an Aadhaar loan?

Yes, in 99% of cases. RBI guidelines for 2026 require PAN for proper credit reporting of any 10000 loan on aadhar card.

Can students apply?

Only if they have a source of income (like a stipend or part-time job). Apps like mPokket specialize in this.

How fast is the approval?

If your e-KYC is successful, a 10000 loan on aadhar card is usually approved within 15 minutes.

Is it RBI safe?

Only if the app is partnered with a registered NBFC. Always check the “About” section of the app.

(This is an estimate based on your provided profile)

Avinash’s Honest Advice

My final word on the 10000 loan on aadhar card is this: It is a bridge, not a permanent solution. Use it only when you have a clear plan to cross that bridge and reach the other side.

The digital lending world in 2026 is fast and convenient, but it has no mercy for those who forget to pay. Check your requirements, compare at least two apps, and read the “Key Fact Statement” before you sign.

Need help choosing an app? Mention your current employment status and city in the comments, and I’ll tell you which lender is currently offering the best rates for a 10000 loan on aadhar card.