- What Is GST on Health Insurance?

- Who Pays GST on Health Insurance? (The 2026 Breakdown)

- GST on Different Types of Health Insurance Policies

- GST Rates on Health Insurance Policies (2026)

- Has GST on Health Insurance Changed Recently?

- How Much Extra Do You Pay Because of GST? (Example)

- Can You Get a GST Refund on Health Insurance?

- Does GST Affect Health Insurance Tax Benefits?

- Should GST Influence Your Policy Choice?

- FAQs – GST on health Insurance

- Deeksha’s Honest Take

Getting the right GST on health insurance details is crucial because it directly impacts your annual out-of-pocket expenses and overall financial planning. With the latest 2026 tax reforms and shifting government mandates, understanding these costs helps you secure the best coverage without overpaying on your premiums.

Let’s be honest: buying health insurance in India often feels like paying a “breathing tax.” You’re already stretched thin by rising hospital bills and skyrocketing premiums. Then, you look at your policy quote and see a massive chunk added as GST.

If you’ve been following the news in late 2025 and early 2026, you’ve probably heard whispers of “0% GST” or total tax removal. But when you go to pay, you might still see a tax component. Confused? You’re not alone.

I’m Deeksha, and I’ve spent years helping consumers navigate the often-murky waters of the insurance industry. My goal isn’t to sell you a policy; it’s to make sure you don’t pay a single rupee more than you legally have to. In this guide, we will strip away the jargon and look at the real impact of GST on health insurance in 2026.

What Is GST on Health Insurance?

GST, or Goods and Services Tax, is an indirect tax levied on the supply of services. Since insurance is categorized as a “financial service,” it has traditionally been taxed under the highest standard slab.

Why insurance premiums attract GST

The government views insurance companies as service providers. When they manage your risk, provide a network of hospitals, and process your claims, they are providing a service. Under the HSN code 997133, this service was historically taxed at 18%.

Current GST rate explained simply

As of early 2026, the landscape has shifted. Following the landmark 56th GST Council meeting, a major reform was enacted:

- Individual & Family Floater Policies: The rate has been slashed from 18% to 0% (Exempt).

- Group Health Insurance (Corporate): These still attract the standard 18% GST.

Is GST charged on full premium or part of it?

For those policies that still attract tax (like group plans), GST is charged on the Base Premium. If you have a “No Claim Bonus” that reduces your base premium, the GST is calculated on that reduced amount. However, if you add “Riders” (like maternity or OPD), the tax treatment depends on whether the rider is bundled into an individual plan (0%) or a group plan (18%).

Who Pays GST on Health Insurance? (The 2026 Breakdown)

This is where most competitors get lazy. They say “everyone pays,” but that’s no longer true. Here is the clear separation:

- Individual Policyholders: If you bought a plan for yourself, you are now Exempt. You pay ₹0 in GST.

- Family Floater Buyers: Similar to individuals, if the policy covers your spouse and children under one umbrella, it is GST-exempt as of the September 2025 reform.

- Senior Citizens: To provide relief to the elderly, the government has ensured that senior citizen specific plans are fully exempt (0%).

- Corporate/Group Holders: If your employer provides your insurance, the company pays 18% GST on the premium. You usually don’t see this unless you are paying for “top-ups” through your payroll.

GST on Different Types of Health Insurance Policies

GST Rates on Health Insurance Policies (2026)

Understanding GST implications on different types of health insurance policies in India

|

Policy Type

|

GST Rate (2026)

|

Status

|

|---|---|---|

|

Individual Health

Personal health insurance policy

|

0%

No GST

|

Exempt

No GST applicable

|

|

Family Floater

Covers entire family under single policy

|

0%

No GST

|

Exempt

GST exempt for families

|

|

Senior Citizen Plans

Special policies for individuals above 60

|

0%

No GST

|

Exempt

Special exemption for seniors

|

|

Top-up / Super Top-up

Additional coverage above base policy

|

0%

Conditional Exempt

|

Exempt (for individuals)

Exempt for individual policyholders

|

|

Corporate Group Plan

Group health insurance by employers

|

18%

GST Applicable

Effective Premium:

Premium + 18% GST

|

Taxable

18% GST applicable

|

Important Notes:

- GST Exemption: Individual, family floater, and senior citizen health insurance policies are completely exempt from GST.

- Corporate Policies: Group health insurance provided by companies attracts 18% GST on the premium.

- Input Tax Credit: Businesses can claim ITC on GST paid for corporate health insurance.

- Renewals: Same GST rates apply during policy renewal as per the initial purchase.

Has GST on Health Insurance Changed Recently?

Yes, and this is the most important section of this article.

What happened in 2025?

In September 2025, the GST Council made a historic recommendation to exempt individual health and life insurance from the 18% tax bracket. This was termed the “Diwali Gift” for the middle class.

What is applicable in 2026?

Today, the exemption is fully active. If you are renewing a policy that you previously paid 18% tax on, your renewal notice should reflect a 0% GST rate.

Truth behind “0% GST” news

Don’t be fooled by headlines that say “Insurance is now free.” The tax is 0%, but the base premium is not. In fact, some insurers slightly increased their base premiums in 2026 to offset the loss of “Input Tax Credit” (money they used to get back from the government). So, while you save 18% on tax, your actual “out-of-pocket” saving might be closer to 14-15%.

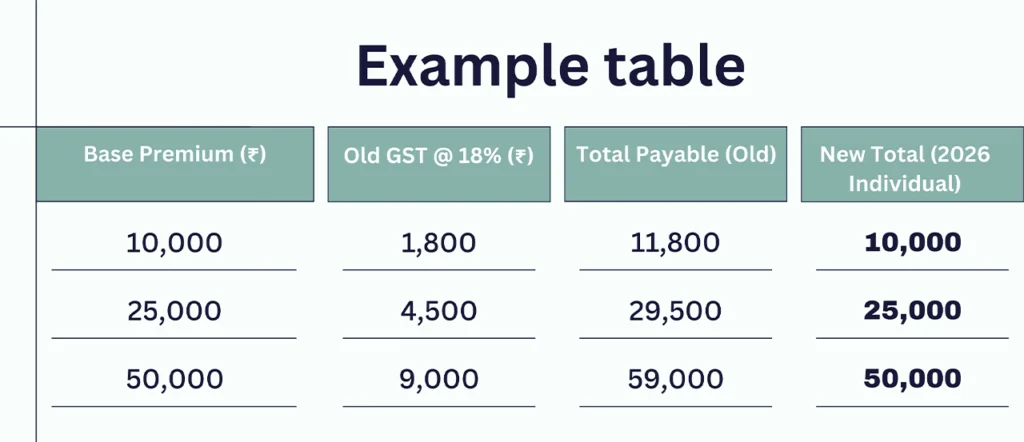

How Much Extra Do You Pay Because of GST? (Example)

Even with exemptions, it’s good to know the math for those still under group plans or looking at historical data.

Note: For individuals, the “Total Payable” is now just the base premium.

Can You Get a GST Refund on Health Insurance?

You can get a GST refund in three specific scenarios:

- Policy Cancellation: If you cancel your policy within the “Free Look Period” (usually 15 days), the insurer must refund the premium and the GST (if any was charged).

- NRIs: Non-Resident Indians paying from an NRE account are often eligible for a GST refund because they are “exporting” the service. They must provide a Tax Residency Certificate (TRC) to claim this.

- Transition Errors: If your insurer accidentally charged 18% GST on an individual policy renewal in early 2026, you can raise a grievance. They are legally bound to refund the excess tax as per the 56th GST Council mandate.

Does GST Affect Health Insurance Tax Benefits?

Yes, but it’s good news. Under Section 80D of the Income Tax Act, you can deduct the premium paid for health insurance from your taxable income.

- The Rule: The entire amount you pay to “keep the policy in force” is deductible.

- The GST Connection: Previously, if you paid ₹20,000 premium + ₹3,600 GST, you could claim the full ₹23,600.

- The 2026 Change: Since the GST is now 0% for individuals, you will simply claim the base premium. You aren’t “losing” a benefit; you’re just paying less upfront.

Should GST Influence Your Policy Choice?

My Honest Advice: Never pick a policy just because of the tax.

- Coverage First: A 0% GST policy that doesn’t cover “Room Rent” or “Daycare Procedures” is a bad investment.

- Corporate vs. Individual: If your company offers a group plan at 18% GST, it might still be cheaper than an individual plan at 0% GST because companies get massive bulk discounts.

Decision Guidance: Calculate the “Net Effective Cost.” If a corporate top-up (with 18% tax) costs ₹5,000 and an individual plan (with 0% tax) costs ₹8,000 stick with the corporate one. The tax is secondary to the total bill.

FAQs – GST on health Insurance

Is GST mandatory on all policies?

As of 2026, it is mandatory only for group/corporate policies. Individual and family plans are exempt.

Do senior citizens get releif GST on Health Insurance?

Yes, they are part of the 0% GST category for individual health insurance.

Is GST the same for all insurers?

GST is a federal tax. Whether you choose Star Health, HDFC Ergo, or LIC, the tax rate (0% or 18%) remains consistent.

Will GST reduce for corporate plans too?

There are ongoing discussions in the GST Council, but as of now, corporate plans remain at 18% to ensure the government maintains some revenue from the sector.

Deeksha’s Honest Take

The removal of GST on Health Insurance is a huge win for the common man. It makes “Insurance for All by 2047” a reachable goal rather than just a slogan. However, stay vigilant. Some insurance companies may try to pad their “Processing Fees” or “Base Premiums” to make up for the 18% tax they are no longer collecting.

Always ask for a “Breakup of Charges” before you pay. If you see a “Tax” line item on an individual policy in 2026, ask why.

Still confused about your premium quote? Paste the breakup in the comments (masking your personal details), and I’ll tell you if you’re being overcharged.