- Can Heart Patients Get Health Insurance in India?

- How Insurance Companies See Heart Patients (The Reality Most Agents Won’t Tell You)

- Heart Conditions vs Insurance Eligibility (At a Glance)

- The Hidden Truth: Insurance After a Heart Event Is Not a Bargain Purchase

- Why This Decision Deserves Slow Thinking

- Types of Health Insurance Options for Heart Patients

- Plan Type Comparison (Reality Check)

- Waiting Period Explained (No Confusion, No Fear)

- What Is Covered for Heart Patients (After Waiting Period)

- What Is NOT Covered (Read This Twice)

- Best Age to Buy Health Insurance After a Heart Diagnosis

- How to Improve Approval Chances (Practical, Tested Tips)

- Common Mistakes Heart Patients Make (And Regret Later)

- FAQs for Health Insurance for Heart Patients

- Does health insurance cover heart surgery after a heart attack?

- Can I buy health insurance if I already have a heart condition?

- What is the waiting period for heart-related claims in India?

- Does health insurance cover the cost of a Heart Stent or Pacemaker?

- Is a medical check-up mandatory for heart patients before buying insurance?

- Deeksha’s Honest Advice (Read This Slowly)

Finding health insurance for heart patients is more than just a financial transaction; it is a promise you make to your loved ones that their future is secure.

A heart-related diagnosis doesn’t just hit the body. It rattles your finances, your family plans, and your sense of security. One day, you are worrying about cholesterol numbers; the next, you’re staring at hospital estimates that look like phone numbers.

In my years of consulting families across India, I’ve seen one pattern repeat itself relentlessly: the insurance confusion becomes bigger than the medical bill itself. People aren’t sure what’s covered, what will be rejected, and whether buying a policy now is even worth the effort.

I’m Deeksha. For over 8 years, I’ve worked closely with individuals navigating health insurance after major medical events, especially cardiac ones. My role has never been to sell hope or push products. It’s to help people avoid expensive mistakes when emotions are running high.

If you are a frequent traveler, it’s very important to know about this travel insurance Comparison, which most people are unaware of.

Here’s my clear promise in this guide:

You’ll understand whether heart patients can get health insurance in India, how insurers really assess risk, and what practical realities you must factor in before paying a single rupee. No fluff. No sales talk. Just clarity.

Can Heart Patients Get Health Insurance in India?

Short answer: Yes.

But, and this is a big but, not everyone gets the same deal.

Insurance companies do offer health insurance for heart patients, but the terms are very different compared to someone with a clean medical slate. Many people assume a flat “yes” or “no.” Reality sits in the grey. Reality sits in the grey, and approval depends on underwriting guidelines defined by the regulator.

Here’s how insurers usually categorize applicants:

- Fresh heart condition (recent diagnosis or surgery)

Approval is difficult. Rejections are common. If approved, expect high premiums and long waiting periods. - Old heart surgery (2–4 years back)

This is where most approvals happen. Terms depend heavily on recovery, reports, and lifestyle changes. - Controlled BP / cholesterol without surgery

Usually accepted under standard or mildly loaded terms.

Most people make the mistake of assuming insurance works like a switch on or off. In truth, it’s more like a dimmer. The light comes on, but not always at full brightness.

How Insurance Companies See Heart Patients (The Reality Most Agents Won’t Tell You)

This is the uncomfortable part. But you deserve honesty.

Insurance companies don’t look at emotions. They look at risk profiling. A heart patient represents a statistically higher probability of future claims. That single fact drives everything premium pricing, waiting periods, exclusions, and sometimes outright rejection.

Medical Underwriting: The Silent Gatekeeper

Before approval, insurers assess:

- Nature of the heart condition

- Time since diagnosis or surgery

- Current medications

- Latest medical reports (ECG, TMT, Echo, lipid profile)

- Lifestyle changes (smoking, alcohol, weight control)

In simple terms, they ask: “Is this person a ticking time bomb or a managed risk?”

Why Premiums Are Higher

Think of insurance like a safety net. If the rope already has frayed edges, the manufacturer charges more. That’s not cruelty, it’s probability math.

Heart patients often face:

- Loading (extra premium)

- Longer waiting periods

- Sub-limits on cardiac procedures

Why Rejection Happens

Rejection usually occurs when:

- The heart event is too recent

- There’s incomplete disclosure

- Reports show unstable markers

- Multiple co-morbidities exist (diabetes + BP + obesity)

Trying to hide facts here is like hiding cracks in a dam. It doesn’t end well.

Heart Conditions vs Insurance Eligibility (At a Glance)

| Heart Condition | Insurance Possible? | Waiting Period |

|---|---|---|

| Angioplasty (2+ years old) | Yes | 2–4 years |

| Bypass Surgery (CABG) | Yes (limited) | 3–4 years |

| Recent Stent Placement | Sometimes | Higher |

| Controlled BP | Yes | Standard |

| Recent Heart Attack | Mostly No | — |

I’ve seen clients waste months applying blindly, only to be rejected repeatedly. Knowing where you stand saves time, money, and morale.

The Hidden Truth: Insurance After a Heart Event Is Not a Bargain Purchase

Here’s an insight many won’t say out loud:

Health insurance for heart patients is about protection, not profit.

You’re unlikely to get:

- Ultra-cheap premiums

- Zero waiting periods

- Unlimited cardiac cover from day one

And that’s okay.

In financial planning, we say: Don’t put all your eggs in one basket. Post-diagnosis, insurance becomes one basket among many alongside emergency funds, lifestyle discipline, and regular monitoring.

The mistake is expecting insurance to undo past medical history. It won’t. What it can do is prevent future hospital bills from bleeding your savings dry.

Why This Decision Deserves Slow Thinking

Heart patients often rush. Fear does that. But rushing into the wrong policy is worse than waiting and choosing wisely.

I’ve watched people buy the cheapest plan available, only to discover later:

- Cardiac procedures were capped

- Room rent limits quietly slashed claim amounts

- Waiting periods reset due to policy changes

Insurance is a long game. Especially after a heart condition.

Types of Health Insurance Options for Heart Patients

Once people accept that health insurance is possible after a heart condition, the next confusion hits: which type of plan actually makes sense? This is where many end up losing money by buying the wrong product.

Let’s break this down cleanly.

Regular Health Insurance (With PED Clause)

This is the most common and most misunderstood option.

A regular health insurance policy covers hospitalization expenses, including heart-related treatments, after the pre-existing disease (PED) waiting period is over.

What this means in real life:

- Heart-related claims are blocked during the waiting period

- Non-heart claims are still allowed

- Coverage continues lifelong if renewed properly

Pros

- Long-term protection

- Covers expensive surgeries like angioplasty and bypass

- Works as a financial safety net in old age

Cons

- Waiting period of 2–4 years for heart conditions

- Sub-limits may apply to cardiac procedures

- Premiums are higher than average

In my experience, this is the foundation policy most heart patients should aim for, provided expectations are realistic.

Critical Illness Plans

This is not a replacement. It’s a supplement.

A critical illness plan pays a lump sum if a listed heart condition occurs, such as a heart attack, bypass surgery, angioplasty, etc. The money comes to you, not the hospital.

Think of it as income protection, not bill reimbursement.

Pros

- One-time lump sum payout

- Money can be used for EMIs, recovery, or lifestyle changes

- No dependency on hospital bills

Cons

- One claim and the policy ends

- Narrow definitions, wording matters

- No coverage for routine hospitalization

I’ve seen families stay afloat financially because this payout kept EMIs running while recovery took months.

Specialized Heart Specific Plans

A few insurers offer heart-focused insurance plans, but tread carefully here.

These plans:

- Cover only heart-related treatments

- Have strict eligibility rules

- Often, cap benefits tightly

Pros

- Shorter waiting period in some cases

- Designed specifically for cardiac care

Cons

- Limited coverage scope

- Not useful for non-heart hospitalizations

- Often discontinued or modified by insurers

These plans work only in very specific situations. They are not a universal solution.

Plan Type Comparison (Reality Check)

| Plan Type | Covers Surgery | Waiting Period | Best For |

|---|---|---|---|

| Regular Health Plan | Yes | Yes | Long-term cover |

| Critical Illness | Lump sum | Yes | Income protection |

| Heart-Specific Plan | Limited | Shorter | Selected cases only |

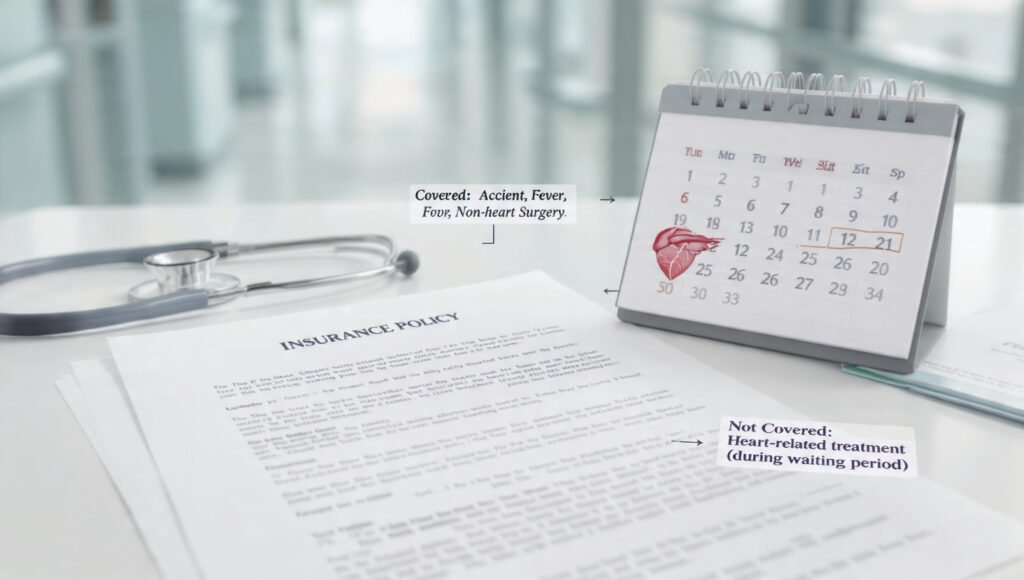

Waiting Period Explained (No Confusion, No Fear)

This is where most people panic, and most agents fail to explain properly.

A PED waiting period does NOT mean your policy is inactive.

It only means:

- Heart-related claims are blocked temporarily

- Everything else continues as normal

What IS Covered During the Waiting Period?

Let’s make this practical.

- Hospitalization due to fever, dengue, typhoid

- Accidental injuries (fractures, stitches, surgery)

- Non-heart surgeries like hernia, appendix, gallstones

I’ve seen heart patients successfully claim lakhs for non-cardiac hospitalizations while their heart waiting period was still running.

What Is NOT Covered?

- Any hospitalization directly linked to the heart condition

- Follow-up heart procedures

- Complications clearly arising from past heart disease

Waiting periods aren’t punishment. They’re risk buffers.

What Is Covered for Heart Patients (After Waiting Period)

Once the waiting period is completed, most standard policies cover:

- Angioplasty and stent placement

- CABG (bypass surgery)

- Pacemaker implantation

- ICU charges and ambulance costs

- Pre- and post-hospitalization expenses

Coverage depends on:

- Sum insured

- Room rent eligibility

- Procedure sub-limits

Ignore these details, and your “₹10 lakh cover” may behave like ₹4 lakh in reality.

What Is NOT Covered (Read This Twice)

This is where claims die.

- Cosmetic or elective procedures

- Undisclosed heart history (instant rejection)

- Claims during PED waiting period

- Policy bought after symptoms appeared but before diagnosis disclosure

Trying to outsmart insurers here is like trying to hide debt from a banker; it catches up.

Best Age to Buy Health Insurance After a Heart Diagnosis

Timing matters more than people think.

The earlier you apply after stabilization, the better your chances.

Why Age Changes Everything

- Younger patients recover faster

- Fewer co-morbidities

- Lower future claim probability

Age vs Approval Chances

| Age Group | Approval Chance | Premium Impact |

|---|---|---|

| Below 40 | High | Moderate |

| 40–55 | Medium | Higher |

| 55+ | Low–Medium | Very High |

I’ve seen two patients with identical heart histories get very different outcomes purely because one applied at 42 and the other waited till 58.

Delay doesn’t improve terms. It usually makes them worse.

Can I get health insurance with a heart condition?

Yes, but with conditions.

Approval depends on:

- Time since diagnosis or surgery

- Stability of reports

- Age and other illnesses

In my consulting work, I’ve seen approvals happen even after bypass surgery, but only when paperwork, disclosure, and expectations were aligned. If someone promises “guaranteed approval,” walk away.

Is a heart stent covered in insurance?

Yes, after the waiting period.

What people don’t realize:

- Stent costs may have sub-limits

- Room rent caps affect total payout

- Consumables may not be fully reimbursed

A stent claim rarely fails outright. It fails partially, and that’s where disappointment creeps in.

Does Bupa / SBI / Star cover heart patients?

There’s no universal yes or no.

Each insurer evaluates:

- Medical history

- Recency of heart event

- Current health markers

I’ve seen the same profile approved by one insurer and rejected by another. This is why blind online purchases are risky for heart patients.

Is heart surgery fully covered?

Technically yes. Practically, it depends.

Full coverage happens only when:

- The waiting period is completed

- No sub-limits apply

- Room rent eligibility matches hospital choice

Otherwise, you pay the gap. Insurance isn’t a blank cheque; it’s a negotiated settlement.

How to Improve Approval Chances (Practical, Tested Tips)

This is where experience beats theory.

1. Full Disclosure, Even If It Hurts

Half-truths are claim killers. Insurers don’t mind heart disease; they mind dishonesty.

2. Keep Medical Reports Ready

Have these scanned and updated:

- Discharge summary

- Angiography / surgery reports

- Latest ECG, Echo, lipid profile

It signals seriousness and transparency.

3. Avoid Instant Online Buys

Algorithms reject what humans might approve. Offline underwriting works better for complex profiles.

4. Use Insurer Medical Checkups

Insurer-conducted tests often carry more weight than external ones. Use them.

These steps don’t guarantee approval, but they dramatically improve odds.

Common Mistakes Heart Patients Make (And Regret Later)

I’m blunt here because these mistakes cost lakhs.

- Hiding medical history

Saves nothing. Destroys claims. - Buying the cheapest plan

Cheap premiums often hide tight sub-limits. - Ignoring room rent caps

This silently slashes reimbursements. - Not reading cardiac sub-limits

“Covered” doesn’t always mean “fully paid.”

Insurance documents are boring. Hospital bills are worse.

FAQs for Health Insurance for Heart Patients

Does health insurance cover heart surgery after a heart attack?

Yes, most comprehensive health insurance plans in India cover heart surgeries like Angioplasty, CABG (Bypass), and Heart Valve Replacement. However, if you already had a heart attack before buying the policy, it will be treated as a Pre-Existing Disease (PED) and will be covered only after a waiting period of 2 to 4 years.

Can I buy health insurance if I already have a heart condition?

Yes, you can. Specialized plans like Care Heart or Star Cardiac Care are specifically designed for people who have already undergone heart surgery or have existing cardiac issues. While the premium might be slightly higher, these plans often have shorter waiting periods (as low as 12-24 months) compared to standard plans.

What is the waiting period for heart-related claims in India?

For a standard health insurance policy, the waiting period for pre-existing heart diseases is usually 3 to 4 years. However, for a heart condition diagnosed after buying the policy, the initial waiting period is only 30 days (except for accidental cases). You can also use ‘PED Waivers’ to reduce this period.

Does health insurance cover the cost of a Heart Stent or Pacemaker?

Yes, the cost of medical implants like stents or pacemakers is covered under the “Medical Devices/Consumables” section of your policy. It is important to check if your plan has any “sub-limits” on the cost of stents, as some older plans cap the amount they pay for these devices.

Is a medical check-up mandatory for heart patients before buying insurance?

Most insurers require a mandatory Pre-Policy Medical Check-up (PPMC) for heart patients or individuals above 45 years. This helps the company assess the current risk. However, some new-age digital plans might offer coverage based on “Tele-MER” (telephonic medical reports) if the condition is stable.

(Ye ek inflation-adjusted estimate hai aapki family ki security ke liye)

Deeksha’s Honest Advice (Read This Slowly)

Health insurance after a heart diagnosis is not about beating the system. It’s about building a safety net that won’t collapse when you need it most.

Don’t rush because of fear.

Don’t chase discounts like cashback offers.

Choose clarity over convenience.

I’ve seen people with “perfect” policies lose money, and others with limited plans survive financially because they understood what they bought.

If you’re confused, pause. Read again. Ask questions. This decision isn’t urgent, but the consequences are permanent.

The bottom line?

Insurance won’t heal your heart. But the right one will protect everything you’ve built around it.

Take this seriously. Your future self is watching.